WHY to raise MONEY-SAVVY kids even if you're struggling with your own finances

AND How to start right now?

3 Steps to implement today

Agenda:

The top 3 common misconceptions about money

How does the brain think about money?

The pros and cons of money beliefs

How to identify your own money beliefs?

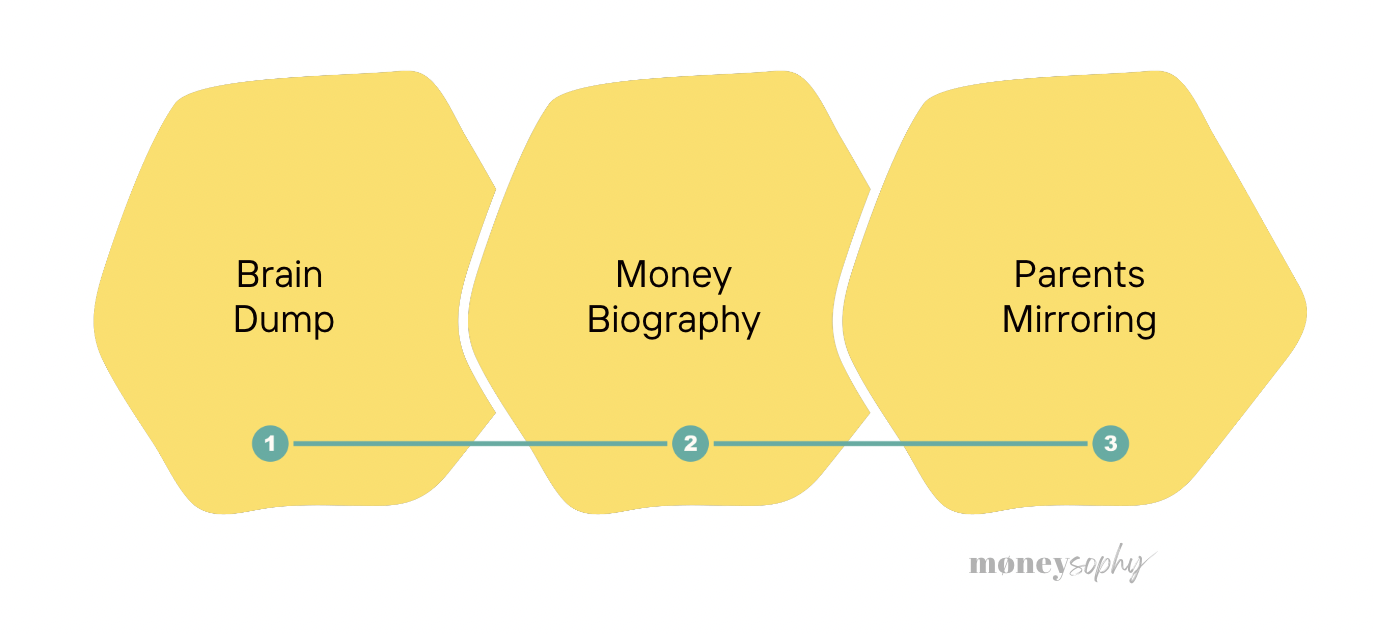

Brain Dump, Money Biography and Parents Mirroring

How to transform your money beliefs?

Key takeaways of Psychology of Money 101

Frequently Asked Questions

The costs of not knowing your money beliefs

In my job, I see many middle-aged clients struggling with their limiting money beliefs and their impact of their parents’ financial actions.

What if we could prevent those issues in the first place?

Here, I explain why and how to talk money with your kids in a healthy way.

The top 3 common misconceptions about PARENTING AND MONEY

#1 “My partner will teach my kid”,

A common belief is the absence of financial education in schools or workplaces is the primary reason for people's struggles with money management. While this belief holds some truth, it doesn't provide the full explanation. Typically you tell yourself “when I have time, I will learn…”, “if I know enough, I will invest…” or “when I invest in this, I will feel at peace”, but how often do these promises ring true in reality?

Some of my clients are trapped in the rabbit hole of personal finances, learning the latest investment trends, always chasing for the highest return. That’s not financial planning, that’s a hobby.

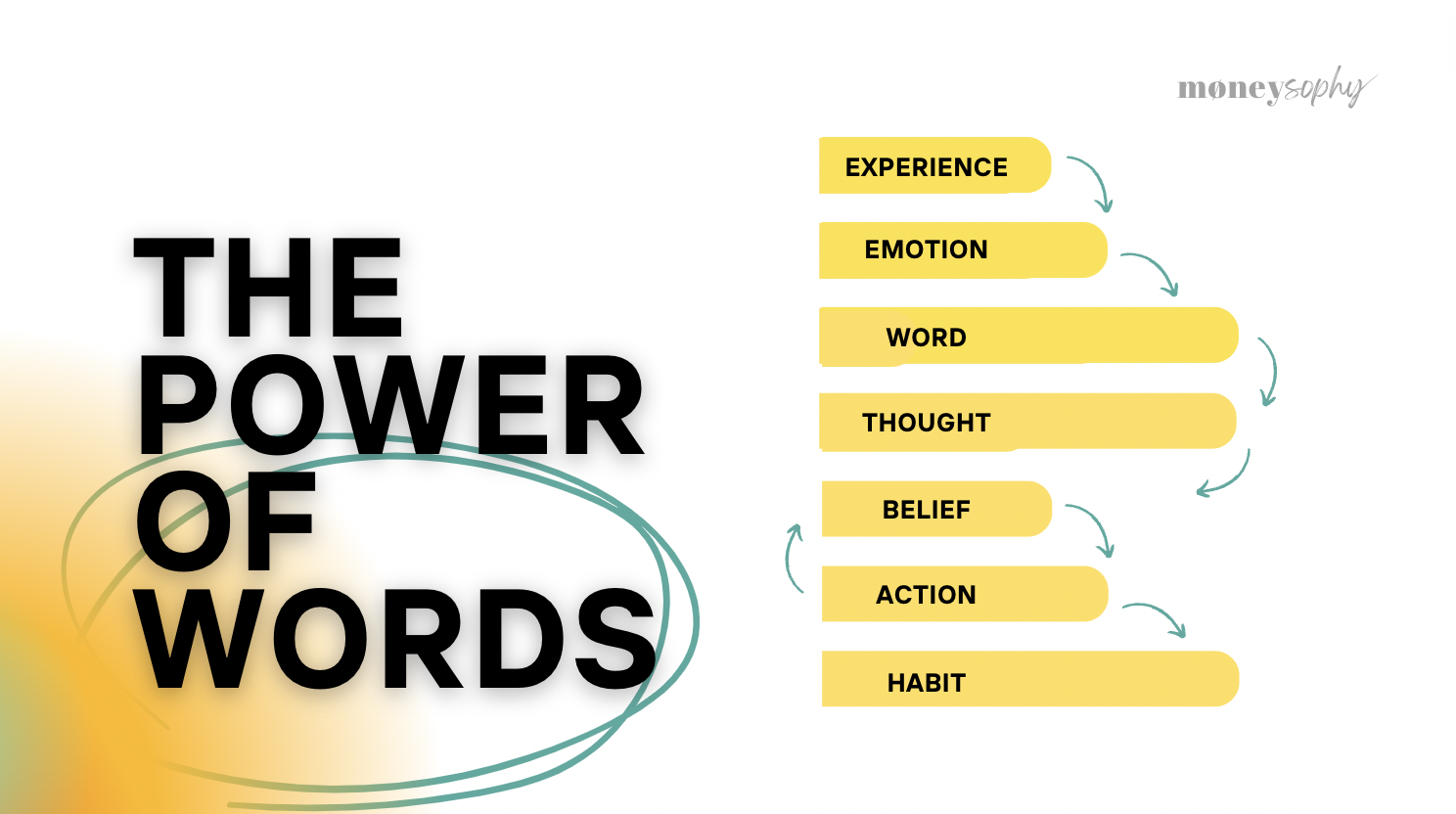

Let me clarify once and for all: money isn’t just about maths, money is emotional.

#2 “My kid will learn later on by themselves”

Yes and no.

Yes, they might,

But if you look at the statistics,

Regardless of your income, I’ve seen clients

#3 “I’m not good with money”

Last but not least, another common belief is that you can just procrastinate, and somehow your money problems will magically vanish as you get older. I often hear “I will start thinking about money later or when I earn x”.

Unfortunately, I have clients in their 50s and 60s who come to me, still grappling with financial anxiety. My conclusion: it’s more challenging to break bad money habits formed for over 40+ years than 10 years.

So no, your personal finances will not miraculously resolve themselves.

And more than that, no one will be as invested in your financial well-being as you are.

why it’s important to start as early as possible?

So why do we say that money is emotional?

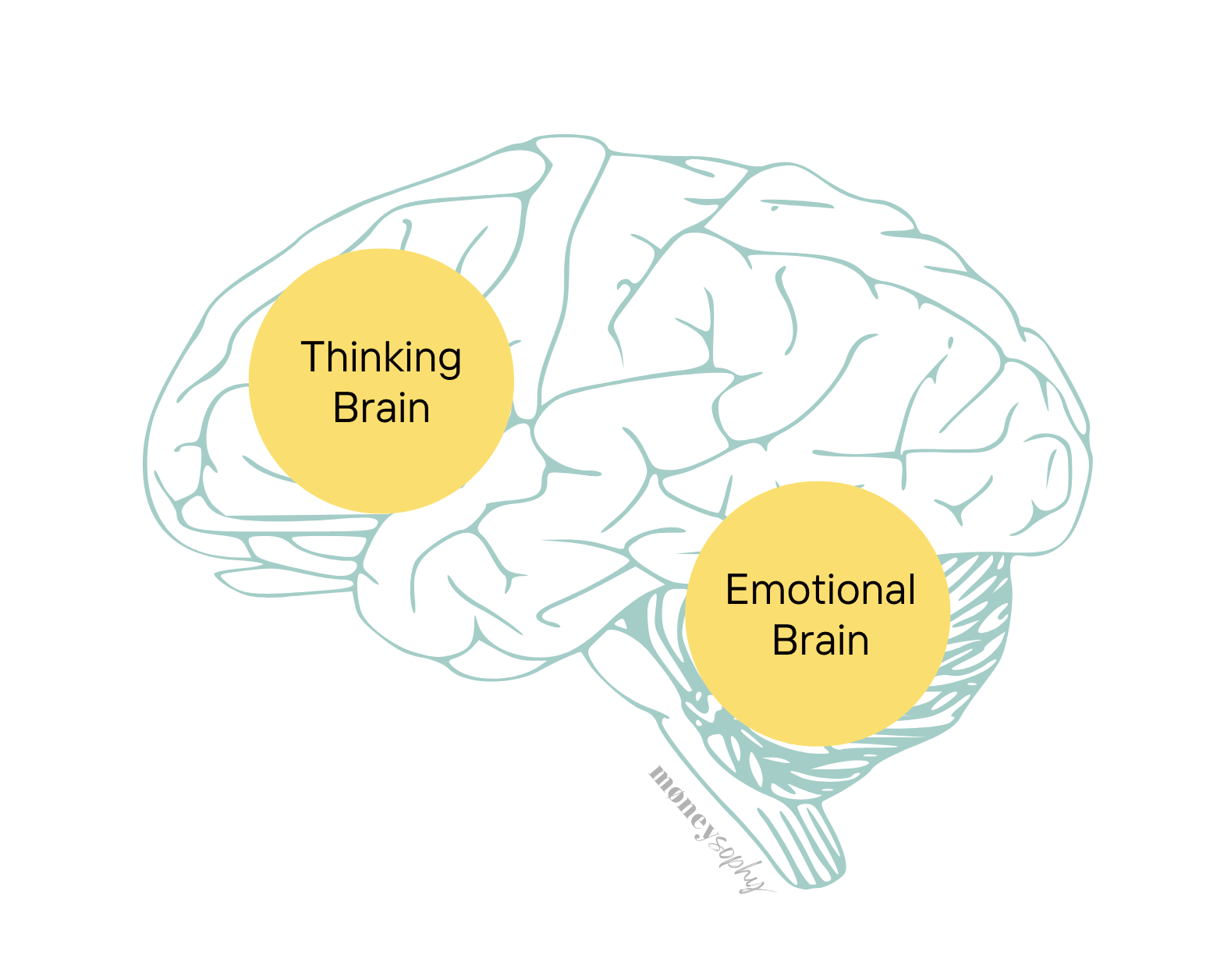

Let’s dive into neuroscience 101 to explain how our brilliant brains think.

Simply put, we have two brains that dictate our behaviours:

The Thinking Brain (Prefrontal Cortex): This is the part of the brain we primarily use when engaged in cognitive tasks. It involves problem-solving, logical reasoning, and operates best when we are in a calm state. Activation of this brain region takes longer but leads to more thoughtful responses.

The Emotional Brain (Limbic System): This brain region generates primal impulses and emotional responses. It is responsible for the fight-flight-freeze response and is often triggered by external stimuli. It reacts quickly, sometimes leading us to engage in actions that we may not fully understand or even regret later.

In many situations, the activation of our emotional brain is not necessarily related to our level of intelligence. Even the smartest individuals can be triggered emotionally and engage in regretful behaviours.

One of the challenges we face is being unaware of our triggers and how to manage the emotions that hijack our thinking brain.

This is particularly common in money-related situations, leading to issues like overspending, financial anxiety, or engaging in speculative investments.

Your emotional brain is also where your past emotions are stored, this also explains why your financial behaviours are the consequences of your experiences.

money beliefs are formed before age 10

Money beliefs are the subconscious attitudes, assumptions, and perceptions we hold about money. These beliefs are often formed in childhood based on our experiences and observations of how our parents and others in our lives handled money.

The money beliefs we develop in our early years can have a significant impact on our financial behaviors and outcomes as adults. Limiting or negative money beliefs can lead to struggles with saving, spending, investing, and overall financial confidence and security.

Many of our core money beliefs are established before the age of 10, as we absorb messages (both implicit and explicit) about the role of money in our family and society. These early-life experiences profoundly shape our relationship with money and can be difficult to change later on

I’ve written down the power of money beliefs in a previous article, you can read it here if you want to find out more about your own (which by the way, will be helpful to see how you behave with your children too!).

Money beliefs can be both permissionless and limiting.

Parents play a big role in shaping the money beliefs of our own children, although not the only actors, but well we can only control what we can.

how do i start talking about money to my kids?

Sometimes, getting started is the hardest.

Let me caveat, there is no point to jumping into investment to your children if you haven’t done the basics yet.

You don’t teach a student complex algebra before talking about simple functions. It’s the exact same with money.

There are equally - if not more - important topics when it comes to talk about money such as family values, spending, goals, vision, needs, wishes…

Now that you know how we including kids formed their money beliefs it’s important to be aware what influence them.

Even though we can’t control everything’s happening in your children’s world (which by the way is a good thing too), you want to be able to control what you can.

First and foremost, become more aware about your own words and your behaviours related to money.

As adults, we hold a lot of money beliefs, we judge something cheap or expensive without realising it based on our values and personal experiences, we behave differently in front of people who are more affluent or lower incomes than us subconsciously…

All these little actions might seem trivial as an adult, but those can have a tremendous impact to our children.

You don’t believe me?

Let’s walk down the memory lane:

Close your eyes, take a deep breath, and replunge to when you were 7-9 years old, what do you hear from your parents? What’s their opinion about buying things? When they buy or didn’t buy you for your birthday? What do they spend a lot in? Or the opposite, what don’t they spend on? What do they complain the most about? What do they praise the most about?

Take your favourite writing tool (pen and paper or else), answer those questions:

Judgment of others:

What do I think of rich people?

How do I

What do I think of poor people?

Judgment of things:

Think outside the box, it doesn’t have to be money pure, it can also be related to objects, studies, …

You can also do the exercise if you’re raising your children with your partner, and challenge each other in the answers.

Secondly, voice up your decision making process.

We take a lot of decisions everyday (around 35,000) and a lot of them it’s financially related:

are we eating out or at home?

should we pick this restaurant or the other one?

Should i order delivery?

Should I take the public transport or the uber?

Should I pick this brand of cookies or this organic one?

Unlike the first one, where it was unintentional, and we say things without conscious, this one is a conscious step.

By voicing up your decision making process, you are sharing your kids not just about money but also:

your values, what you care the most about in your family (health, exercising, sharing, respectfulness,….)

the importance to follow a budget, you have x amount dedicated in a specific category (discipline, self-commitment, budgeting, …)

tools to make a choice (giving them prompts to simplify their decision making process later on in life)

Thirdly and finally, delay instant gratification in all sorts.

We live in an attention economy where everything is about having everything right NOW.

Don’t know what to cook tonight? Google a new recipe.

Don’t know how to fix your leaking tape, watch a Youtube video.

Get bored? Watch some Tiktok dancers or funny cat videos.

Want to see what your friends up to? Stalk them on Instagram stories.

Craving for Chinese good? Get Deliveroo.

You see the whole picture.

While our generation might not have fully grown up with the Internet culture, our kids are diving since they were born (simply walk in a restaurant and count how many toddlers are watching Youtube in their parent’s phone).

I’m not here to diabolise the Internet.

The problem is a lot of those apps have been designed to be addictive Addiction by Design + center for humane technology.

In fact, Aza Rasking, the inventor of the infinite scroll told the media it’s his biggest regret in life.

“One of my lessons from infinite scroll: that optimizing something for ease-of-use does not mean best for the user or humanity.”

- Aza Raskin

Ok, so why it’s related to money? EVerything is interconnected.

The reason why I See so many middle age clients struggling to meet their ends meet, it’s because those luxuries wishes have all became a need for them.

they can’t dissociate the wants versus the needs.

We always want more, regardless of the income level. I have clients who earn more than $150,000 USD a year without dependents, adn they still live paycheck to paychgeck struggling to keep up with their fancy lifestyle.

Concretly, how can you help your kids to delay gratification, here are a few examples:

help them flex their patience muscle before getting waht they want (toy, clothes, activity…): In neurosciences, creating desire gives you more dopamine, the ‘reward’ neurotransmitteur in your brain. In other words, having a desire to get something gives you more pleasure than actually getting the actual thing.

ask them in-depth questions

Let's kick off with the first exercise: Brain Dump.

Sure, you might be aware of some of the obvious money beliefs, like the ones you often heard your parents repeating. But we're going to dig deeper.

Grab a pen and paper or your favourite note writing app, and without any filter or holding back, jot down the very first things that come to mind when you think about money.

This is your opportunity to empty your mind. No filter, no holding back. Get it all out on paper.

One you finish the list, ask yourself: is there anything else missing?

If you want to take a step further, you can self analyse your money beliefs by assessing whether they are falling into a money disorder category - which is a term coined by Brad Klontz and Ted Klontz in their book Mind over Money.

Money disorders are these persistent, predictable patterns of self-destructive financial behaviours that wreak havoc in our lives. They bring along heaps of stress, anxiety, emotional distress, and seriously mess things up in major areas of our existence.

Here are the three types of common money disorders:

At each stage, their learning

Let's dive into the third and final exercise: Parents Mirroring.

This exercise aims to shed light on the financial behaviours that have been passed down to you by your parents or caregivers.

It's fascinating how we, as kids, are like sponges, absorbing everything we see and hear. Without even realising it, we subconsciously imitate our caregivers or the opposite. Some of the behaviours we exhibit are a result of our unique personalities.

Draw a table with different columns. Each column represents a caregiver that has been omnipresent in your childhood. Perhaps your parents, uncles, aunts, a grandparent etc.

Now, close your eyes, and take a moment to reflect on each of your caregivers’ financial tendencies.

List every adjective or sentence that comes to your mind related to their financial behaviours. It could be something they did or said often.

Are they more of a spender or a saver? Are they a hard worker or a risk-taker? What is their relationship with money? What do they say about rich people or poor people? What is the thing you noticed about them when you were young?

Then once you finish their lists, draw a last column which is yourself, and do the same exercise.

Now you have a clear picture of your money patterns. Highlight the ones that are “inherited” by your caregivers and circle the ones you’ve manifested on your own. By identifying which behaviours originated from whom, you can gain a better understanding of the origins of your own financial behaviours. It's like piecing together the puzzle of your money mindset.

How TO TRANSFORM my money beliefs?

Here you go, you have now identified all your money beliefs, you can move to the next stage which is to let go of money beliefs that no longer serve you.

There are 4 main stages to transform your money beliefs.

Last but not least, leading by example is probably the best thing you can do

Key takeaways PaRENTING x MONEY

Recognise that personal finances is more than just mathematics.

80% is psychology, while only 20% is financial education.

Our childhood experiences directly influence our financial behaviours today.

Beliefs hold immense power, shaping our lives, studies, careers, and relationships.

By changing your words, you can gradually shift your perception and mindset.

Your past has shaped your current money beliefs.

With consistency and persistence, you have the power to transform those beliefs.

Transforming your money beliefs is a journey, learn to appreciate the ups and downs rather than solely focusing on the end results.

Frequently Asked Questions

-

When it comes to changing deeply ingrained money beliefs, it can definitely be a challenge but not impossible.

One strategy you can try is exploring your money triggers. Pay close attention to situations or topics that evoke strong emotions or reactions related to money. These triggers can often provide valuable clues about your deep-seated beliefs and fears. By examining your emotional responses, you can gain insight into the underlying beliefs that drive them.

Another option to consider is working with a Money Coach. Professionnals can offer guidance and support as you navigate the process of transforming your money behaviours. They have specific exercises and techniques that can help you delve deeper into your mindset and uncover the beliefs that may be holding you back. Feel free to book a call here with me to engage the conversation.

Remember, changing your money beliefs is a personal journey, and it may take time and effort. But with self-reflection, exploration of triggers, and the assistance of a professional, you can make progress in transforming your relationship with money.

-

Identifying your money beliefs is a gradual and ongoing process. Be patient with yourself and approach it with curiosity and an open mind. As you delve deeper into your relationship with money, you'll gain clarity and a better understanding of your beliefs.

Here are a couple of perspectives and strategies to consider:

Patience and Self-Compassion: Changing money beliefs takes time and self-compassion. Be patient with yourself and understand that resistance is normal. Embrace the process as an opportunity for personal growth and self-discovery. Remember, you don't have to tackle everything at once. Take your time and work on it gradually over the next few weeks.

Seek Support: Consider seeking support from your partner or a friend. Discussing your money beliefs with others can provide fresh insights and help you challenge any limiting beliefs.

Alternatively, you can also grab a virtual coffee chat with me (click here to book a FREE call) to identify blind spots you may not see on your own.

-

If you find yourself feeling stressed despite having a solid financial plan in place, it's important to recognize that the root of your stress may not lie solely in your financial solutions. In many cases, the underlying issues are emotional or psychological in nature.

Regardless of the level of financial planning you have undertaken, you may still experience stress if there are deeper emotional or psychological challenges at play. Money-related stress often stems from a variety of factors such as fears, limiting beliefs, past experiences, or even relationship dynamics.

In such situations, it's beneficial to seek professional help from a therapist, counsellor, or money coach who can provide guidance tailored to your specific situation. These professionals are trained to help you explore and address the emotional aspects that contribute to your stress. They can assist you in developing coping mechanisms and strategies that go beyond financial planning, helping you build resilience and manage stress more effectively.

-

First and foremost, it's important to remember that differing financial perspectives within a relationship are quite common. We all have unique backgrounds, experiences, and beliefs when it comes to money. The key lies in finding common ground and establishing open and honest communication.

Here are a few steps you can take to navigate this situation:

Open Dialogue: Initiate a calm and respectful conversation with your partner about your financial planning and money beliefs. Create a safe space where both of you can express your thoughts, concerns, and aspirations. Listen actively to understand each other's perspectives without judgment.

You can kickstart the conversation with: What does money mean to you? How was it growing up in your family financially?

Identify Common Goals: Discover shared financial goals that you both can strive towards. It could be saving for a down payment, planning for retirement, or even funding a dream vacation. Finding common ground and aligning your goals can help create a sense of unity and purpose.

You can kickstart the conversation with: How do you see ourselves in 5 and in 10 years? If we win the lottery tomorrow, how would you live your life differently?

-

Item description

WHAT’s NEXT?

If you have applied everything shared in this page, congratulations!

Most people are not aware of their limiting money beliefs. So you are already doing better than 90% of people.

So, what's next? Continue practicing your newly acquired financial habits, enhance your financial planning skills, and consistently work towards building your wealth both in a literal and figurative sense.

Additionally, you might find it beneficial to establish a solid payday routine, aka the 6Ps, to further support your financial journey.

Lastly, leading by example is probably the best you can do for your children.

__

Do you find it challenging to get started?

Remember, you don't have to navigate this journey alone! I invite you to book a FREE call with me here or sign up for our Money Made Easy Cohort, where we can discuss your main roadblocks and work together to overcome them.

If you believe that you are experiencing deeper issues, severe addiction, or other mental health concerns, it is important not to isolate yourself. Reach out for professional mental health support in your area.

The costs of not talking about money to your children

If you don’t prepare your kids for their future, your kid might…

repeat the same financial mistakes that you did

develop an unhealthy relationship with money

be stuck in a toxic relationship/job because they can’t afford to leave

have limiting goals because of the lack of financial confidence

have low self-esteem

fall into any type of addiction (shopping, gambling, …)

have no financial empowerment